a) Reconciliation of irregular expenditure

Irregular expenditure condoned by the National Treasury in line with the guidelines issued.

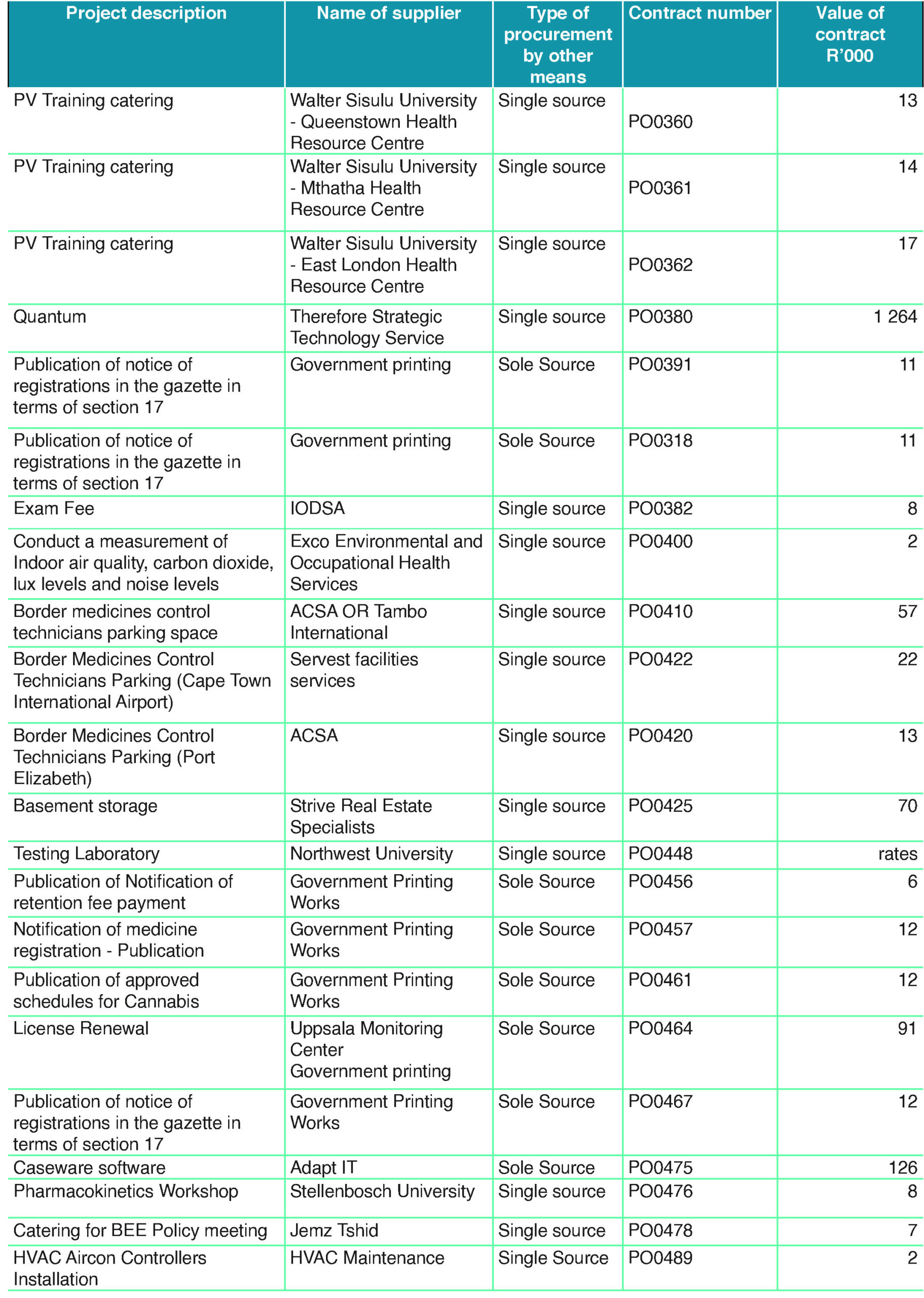

b) Details of current and previous year irregular expenditure (under assessment, determination, and investigation)

SAHPRA does not have any unconfirmed irregular expenditure

c) Details of current and previous year irregular expenditure condoned

Irregular expenditure condoned by the National Treasury in line with the guidelines issued

d) Details of current and previous year irregular expenditure removed – (not condoned)

All irregular expenditure confirmed were subsequently condoned by the National Treasury

e) Details of current and previous year irregular expenditure recovered

No irregular expenditure confirmed required recovery in line with the National Treasury guidelines

f) Details of current and previous year irregular expenditure written off (irrecoverable)

No irregular expenditure was identified for recovery or required to be written off

g) Details of current and previous year disciplinary or criminal steps taken as a result of irregular expenditure

Disciplinary action appears to be effective as subsequent similar transgressions were not noted.

a) Reconciliation of fruitless and wasteful expenditure

Additional fruitless and wasteful expenditure identified during the 2022/23 financial year related to interest and penalties issued by SARS due to under-payment of PAYE. A determination test was completed, which did not recommend recovery against liable officials and was subsequently written off.

b) Details of current and previous years fruitless and wasteful expenditure (under assessment, determination, and investigation)

SAHPRA does not have any unconfirmed fruitless and wasteful expenditure

c) Details of current and previous year fruitless and wasteful expenditure recovered

d) Details of current and previous year fruitless and wasteful expenditure not recovered and written off

A determination was conducted and found no liable official due to resignations as well as unforeseen system error resulting in late payment penalties and interest being written off

e) Details of current and previous year disciplinary or criminal steps taken as a result of fruitless and wasteful expenditure

a) Details of current and previous year material losses through criminal conduct

No material losses identified

b) Details of other material losses

Invoices paid after 30 days or agreed period due to queries raised with the service provider or internally for correction/clarification before payment was processed.

Older than 30 days (unpaid and in dispute) is mainly due to queries raised with service providers not as yet resolved.